We are now entering a long period of hyperinflationary depression which will mark the ignominious end of the latest and most catastrophic fiat experiment in the history of the world.

The seeds of the impending catastrophe were sown with the creation of the Federal Reserve in 1913, a private bank whose power grew and grew over the years until it became the effective government of the US and some would say by extension the world. Its power was magnified further when in 1971 it eliminated the necessity to have any gold backing for the dollar and with the establishment of the petrodollar. The global dollar ponzi scheme expanded exponentially to arrive at the point we are at now, where the dollar is intrinsically worthless, it’s just that most of the world hasn’t figured that out yet.

By the end of 2019, a year characterized by mounting discontent and demonstrations around the world, it was apparent that this ponzi scheme had almost hit the buffers, with the appearance of the repo crisis in the Fall of that year. Something drastic had to be done to provide the excuse to create trillions more dollars so that the can could be kicked a few more years down the road. Enter the Covid scamdemic, which made it politically possible to indulge in “emergency funding” on a grand scale. The Covid scamdemic also afforded numerous other other benefits such as the opportunity to cull the population, especially the elderly whose pension demands could never be met, via the “virus” and the “vaccines” to treat it, which were both created in labs and a window of opportunity to get the global population trained up for eventual Martial Law when the world economy completely collapses by means of so-called “Lockdowns”.

It’s important also to understand that, in addition to the enormous inflationary pressures resulting from profligate money creation, there are powerful deflationary forces at work at the same time – hardly surprising considering that the world economy is collapsing with sagging consumer demand as a result of inflation and rising rates and massive supply chain disruptions and sabotage of vital infrastructure and the food supply etc. However, these deflationary pressures are being masked by the massive money creation, not just by the Fed but by Central Banks all over the world. This is why, in its quest to achieve zero purchasing power, the dollar has some serious competition from other currencies vying for the coveted prize of the currency that can get to being worthless first. So although the dollar is heading in the direction of worthlessness, the dollar index, which is a measure of the dollar relative to other currencies, can actually rise, and a supporting factor for the dollar that we should keep in mind is the need for other countries around the world that are grappling with mountains of dollar denominated debt, often courtesy of the IMF, to pay back or at least service these debts.

In the face of this accelerating race to the bottom by most global fiat that will end up worthless, it is imperative that investors and citizens generally striving to conserve the purchasing power of whatever wealth they have move their capital to something that will maintain its value, and with respect to this there is no better store of value than gold and silver.

Gold always retains its intrinsic value, no matter what, so in a sense its price in fiat is irrelevant – it only matters to the extent that if you time your purchases well you can swap more fiat garbage money into it. Silver’s advantage meanwhile is that in a situation where paper money is worthless or close to worthless you can use it for relatively modest transactions. If you try to use gold you might be shot or clubbed and have the gold stolen, especially in the Mad Max world that is now emerging, that’s less likely with a silver coin.

Taking all this into consideration, especially the recent ramping up of inflation, it may seen strange that gold and silver’s paper price has still not risen above their highs of mid-2020, almost 3 years later. Here we should factor in that the paper price of gold and especially silver is rigged – you go try and buy a quantity of physical gold and silver at the paper price and see how far you get. Apparently J P Morgan controls more than 50% of the paper silver market, and demand for physical silver is now at record levels although you wouldn’t think so looking at the paper price and demand is set to continue to grow rapidly. If there was true price discovery in these markets the prices would be much higher and there wouldn’t be shortages, it’s that simple. What this means is that we are effectively seeing “price fixing” of the sort you see in communist style command economies, which creates shortages and a black market. Unless they stop rigging these markets we can expect to see a thriving black market start to flourish in gold and silver as demand pressures build, regulation or not, that will eventually render those attempting to rig their price as impotent and sidelined.

Now we will proceed to “play the paper game” like most others and see if we can figure what is likely to happen to gold priced in dollars over the medium and long-term especially. As far as gold itself is concerned we aren’t minded to sell, except on a trading basis, as the emphasis is more on adding to positions on dips. The paper price fluctuations of gold and silver of course become much more important when it comes to timing decisions with respect to trading gold and silver stocks, as if we can reduce positions at peaks and add to positions on dips we can greatly improve our performance.

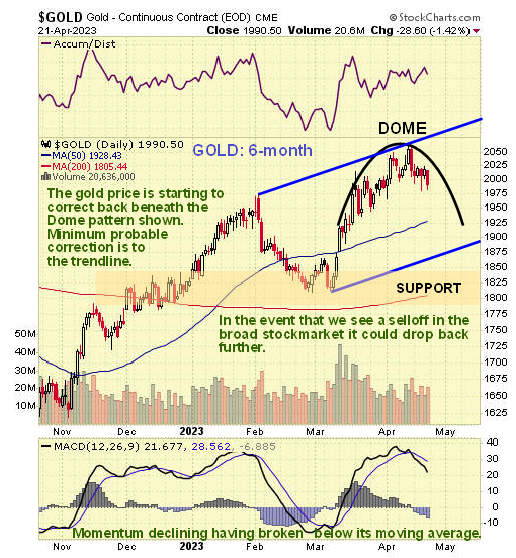

On the 6-month gold chart we can see that, following a wave up during March and into April that resulted in a substantially overbought condition on its MACD, gold has rolled over beneath a Dome pattern and is starting to correct back. There are various targets for this correction depending on what the broad stockmarket does, but at the least it looks likely to drop back to the lower boundary of the prospective channel shown, whose boundaries are at this point not definite, and it could fall further to the support level beneath.

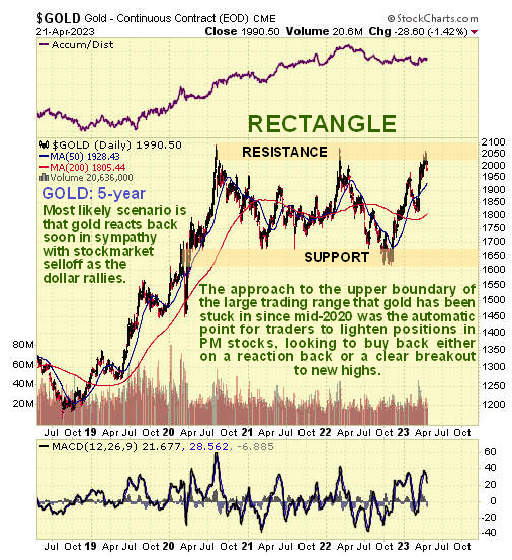

On gold’s 5-year chart we see at once why it would correct back from this level, since it had arrived at resistance at the top of the large Rectangular trading range that formed from mid-2020 to the present. Gold’s performance from mid-2020 is unimpressive, since taking inflation into account, which is now robust, it is of course down. Tactics here are to reduce holdings with the aim of building them back on a signficant correction, or hedge them, which we have already done, or alternatively to add to positions on a clear breakout above the resistance, should that happen, which at this point doesn’t look likely.

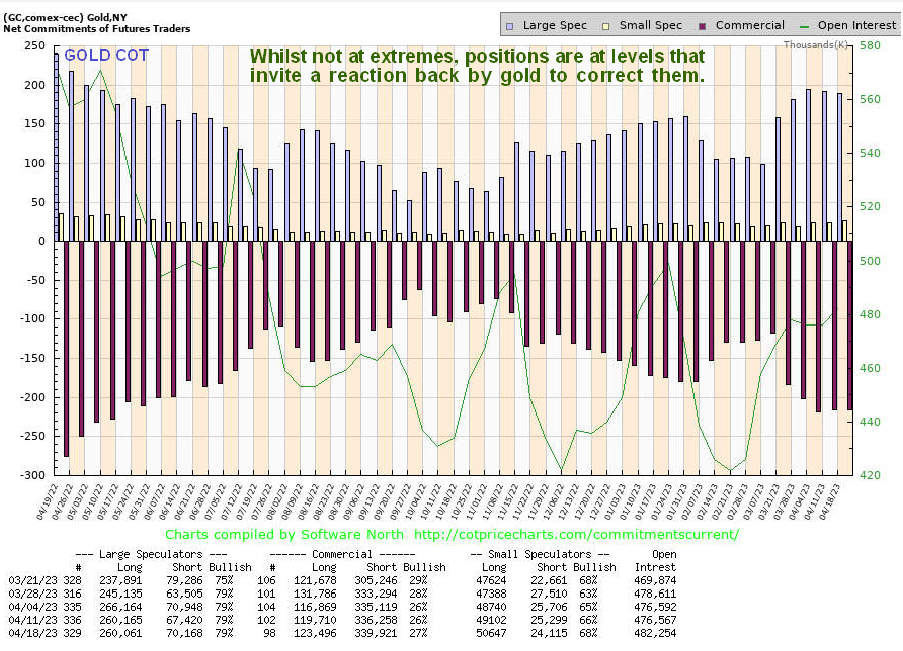

Gold’s latest COT chart shows that ,while there is room for further gains, it looks more likely to react than to advance over the short to medium-term.

On the 5-year chart for GDX we can see that unlike gold, it hasn’t gotten up to the resistance at its 2020 and 2022 highs, showing a lack of conviction and skepticism that is actually bullish, although that said, if gold drops away here, as it look like it’s going to, it will take the stocks down with it.

Now we come to a useful chart which plots the performance of Precious Metals stocks relative to the S&P500 index. It shows us that PM stocks have outperformed the broad market on the recent rally from early March but more importantly this chart reveals that PM stocks have been slavishly moving with the broad market for much of this year. The conclusion from this is that if the broad market takes a hit soon – and we are talking about a drop, not a crash – it will take the PM sector down with it. So the next question is “How does the broad stockmarket look?”

On the 1-year chart for the S&P500 index we can see that its broad trend is sideways at this point, and it is suspected that the rally from the October lows through early February may have been nothing more than a bearmarket rally, although what happens next probably depends on how much new money the Fed is prepared to create and its stance on rates. A retreat from here does look likely, because the market is close to resistance at the February highs and somewhat overbought on its MACD, and if it does retreat, going on past behaviour, it looks likely that the PM sector will drop with it.

Lastly, it is important that we look at the US dollar index, especially as it is right now at a critical juncture. On the 2-year chart we see that, following a strong bullmarket phase during the last half of 2021 which lasted well into 2022, it has reacted back quite hard, which at this stage may be nothing more than a heavy correction. Over the past month or two there has been no shortage of people reading the dollar its last rites on account of BRICS members declaring their intention to move away from using the dollar, with a bombshell development being Saudi Arabia accepting Yuan payments for oil, and all this doubtless accounts for a large part of recent dollar weakness, but the international dollar market is vast and it is not going to fall into disuse overnight, it will take time, kind of like a slow motion train wreck. What could happen here as a result of painfully high interest rates (by recent standards) is that dollar debtors scramble to buy dollars to pay back / pay down debt thus triggering a dollar rally feedback loop, and we can see on our chart that the dollar index looks like it might be at the 2nd low of a Double Bottom and if it is, a big rally could be in the offing that would clobber commodity prices, gold and silver included. So clearly, what the dollar does next is of key importance.

End of update.